Mexico: Economic Outlook for 2023 and 2024 (Updated as of the 1st semester of 2023) It is projected that the real Gross Domestic Product (GDP) growth will experience a slowdown, declining from 2.5% this year to 1.6% in 2023, although a rebound to 2.1% is expected in 2024.

Consumer spending will be supported by the gradual improvement of the labor market, albeit weakened by high inflation. On the other hand, exports will continue to benefit from their high integration in value chains, although their dynamism will be affected by the deceleration in the United States. Inflation is expected to decrease to 5.7% in 2023 and 3.3% in 2024.

To address the increase in energy prices, it is necessary to focus on the most affected households and small and medium-sized enterprises, offering incentives for energy savings. In terms of monetary policy, a restrictive stance must be maintained to anchor inflation expectations. Having competition defense authorities and independent regulators with sufficient funding would contribute to boosting competition and productivity. Additionally, improving access to and the quality of childcare services would promote women's labor force participation and reduce educational inequalities.

The prospects for economic activity are worsening, and inflationary pressures remain high. After strong growth in the first three quarters of 2022, high-frequency indicators show a decline in activity in some sectors. Recently, production in the mining and construction sectors has contracted, although automobile production has managed to withstand thanks to supply chain improvements. Although external demand has remained resilient, it is expected to weaken as growth in the United States slows down. Inflationary pressures remain high and widespread, with a general and underlying inflation of 8.4% (year-on-year) in October. Moreover, medium-term inflation expectations have increased.

Fiscal policy remains prudent, and monetary policy will need to remain restrictive.

Fiscal policy remains prudent, and monetary policy will need to remain restrictive. With the aim of reducing cost pressures and supporting households' purchasing power, a mechanism to stabilize retail fuel prices has been implemented. According to estimates, this is reducing inflation by 2% to 4%. The budgetary cost associated with this mechanism is estimated at 1.4% of GDP in 2022. It is expected that this mechanism will be maintained during the projected period. Increased oil revenues will cover the cost of the stabilization mechanism, but a greater impact of international fuel price fluctuations on national retail prices would reduce the future budgetary cost of the mechanism and provide better incentives for energy savings. This would allow for some fiscal flexibility to strengthen social programs and provide more targeted support to vulnerable households.

Furthermore, the government is taking measures to mitigate pressures on commodity prices, such as the temporary elimination of import tariffs on essential products, cooperation with the private sector to freeze the prices of 24 key products (mainly food) for six months, and adopting measures to increase basic grain production. Fiscal policy remains prudent and continues to prioritize some social programs, especially non-contributory pensions, and priority infrastructure projects in the southern region of the country. The budget deficit is estimated to increase to 3.6% of GDP in 2023, up from 3% in 2022, and the official measure of public debt will stabilize at around 50% of GDP. Mexico has also begun rebuilding fiscal reserves, gradually replenishing the stabilization fund, which now has resources equivalent to 0.1% of GDP. This is a prudent measure to enhance responsiveness to sudden negative disruptions.

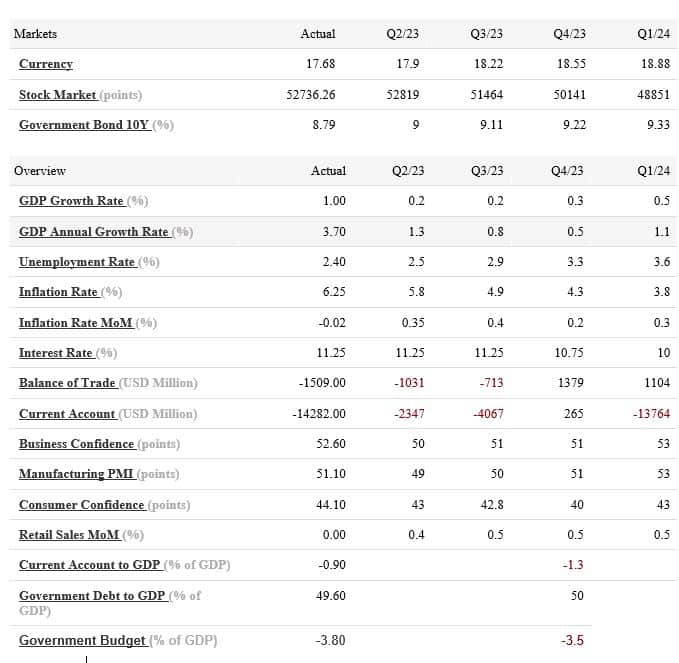

In response to rising inflationary pressures and to anchor inflation expectations, the Central Bank has gradually increased the official interest rate to 10%. Given the prospect of persistent generalized price pressures, further interest rate hikes would be justified. Projections indicate that the official interest rate will rise to 10.

Moderate growth is expected, and increasing productivity is a key priority

Se proyecta un crecimiento económico moderado del 1,6% en 2023 y del 2,1% en 2024, ligeramente por encima de su potencial. El impulso principal vendrá del consumo interno, mientras que los servicios relacionados con el turismo se irán recuperando de forma gradual. Las exportaciones continuarán beneficiándose de su profunda integración en las cadenas de valor del sector manufacturero, especialmente en las industrias electrónica y automotriz, aunque se verán afectadas negativamente por la desaceleración del crecimiento en los principales socios comerciales. La inflación se moderará gradualmente en 2023 y 2024, a medida que el impacto del aumento de las tasas de interés surta efecto y la capacidad ociosa limitada ejerza presiones salariales contenidas. No obstante, las perspectivas de inflación aún presentan incertidumbre significativa. Existe la posibilidad de que la inflación se mantenga en niveles más altos durante un período prolongado, lo cual erosionaría el poder adquisitivo, especialmente de las familias vulnerables, y requeriría una política monetaria más restrictiva. Episodios de volatilidad financiera podrían aumentar la aversión al riesgo, reducir los flujos financieros netos y elevar los costos de financiamiento. Por otro lado, la aceleración del fenómeno de «deslocalización cercana» (nearshoring) de procesos de producción hacia México, con el fin de facilitar el acceso al mercado estadounidense, podría generar un aumento en las exportaciones.

Increasing productivity is a key priority in this context. Expanding the tax base would contribute to addressing the growing expenditure needs in education, healthcare, and infrastructure, ensuring debt sustainability while fostering productivity and growth. Reducing the costs associated with regulations in the process of business formalization, particularly at the subnational level, and further improving mechanisms for labor dispute resolution would support the strengthening of formal employment. Allocating more resources to primary education would mitigate the adverse effects of the pandemic on educational outcomes. Additionally, promoting urban and interurban public transportation, as well as encouraging the use of renewable energies, would contribute to reducing emissions and decreasing dependence on fossil fuels.

References

{kind=link}

{kind=link}

Leave A Comment